We are pleased to present the November 2025 edition of Financial Reporting Update, in this edition we will look at:

- New requirements for 31 December 2025 reporting entities.

- AASB post-implementation review update

- Regulatory focus

- Control and consolidation

- Accounting position papers

New requirements for 31 December 2025

The good news for preparers of 31 December 2025 financial statements is that there is only one new accounting standard. The even better news is that this standard is unlikely to be relevant for many of you.

AASB 2023-5 Amendments to Australian Accounting Standards – Lack of Exchangeability provides clarity and additional guidance for entities who transact in hyperinflationary currencies.

We note that the International Interpretations Committee has also released an agenda decision to assist entities in assessing whether a currency is hyperinflationary.

The current hyperinflationary economies are:

| Argentina | Sierra Leone |

| Burundi | South Sudan |

| Haiti | Sudan |

| Iran | Turkiye (Turkey) |

| Lebanon | Venezuela |

| Malawi | Zimbabwe |

AASB NFP post-implementation review (PIR) updates

In 2022, the Australian Accounting Standards Board (AASB) commenced its PIR of Australian amendments to certain accounting standards relating to NFP and public sector entities. The topics included:

- Control and consolidation for NFP entities

- The definition of a structured entity for NFP entities

- Related party disclosures by NFP public sector entities and

- Disclosures in special purpose financial statements regarding compliance with Australian Accounting Standards.

In October 2025, the AASB released their feedback statement which completes this project. This concluded that the NFP requirements were ‘generally working as intended’ although there may be ‘opportunities to improve aspects of some of the requirements’, however this will depend on future evidence gathering and availability in the AASB workplan.

We would not expect any significant changes to these requirements in the Australian Accounting Standards and encourage our NFP clients to ensure that NFP specific requirements are used in applying the standards.

Areas of ASIC attention

ASIC have certainly been busy in the external reporting space since our previous newsletter, and they have released a number of documents of interest.

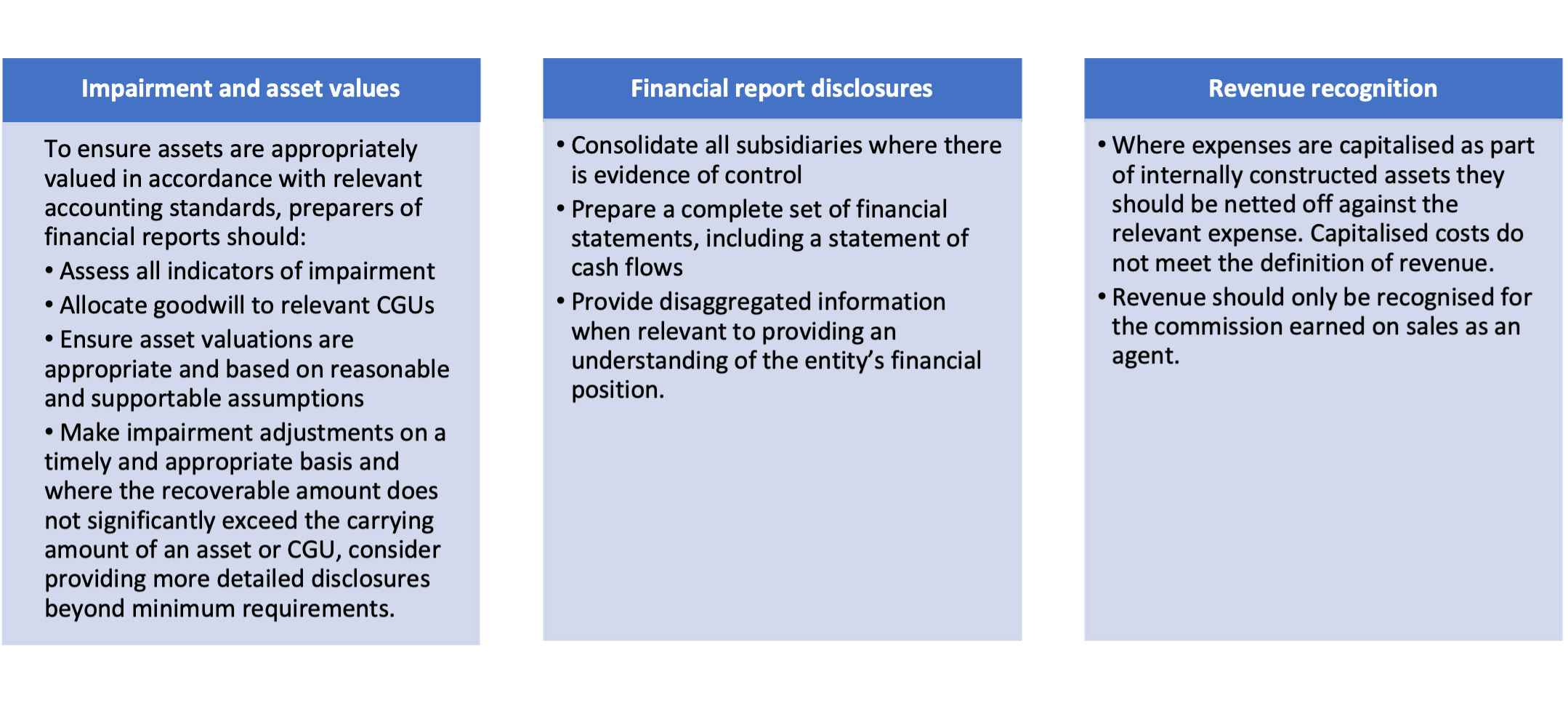

Report 819 ASIC’s oversight of financial reporting and audit 2024-25

This report was released in October 2025 and provides information about ASIC’s recent reviews of financial statements, audit files and voluntary sustainability disclosures.

The diagram below summarises their findings from financial statements:

The ones most relevant to our clients relates to impairment, disclosures and revenue recognition and ASIC have provided more guidance for preparers on these topics.

Non-lodgement of financial statements

ASIC have released a number of media releases in relation to non-lodgement of financial statements by proprietary companies (25-141MR, 25-169MR and 25-239MR) and have stated that financial reporting misconduct including failure to lodge financial reports is one of their 2026 enforcement priorities (25-273MR).

ASIC has issued letters to some entities requesting clarification around their size classification and whether they have met their financial reporting obligations under the Corporations Act.

This is reminder for all entities to review their obligations around the preparation, audit, and lodgement of financial reports with the appropriate regulator.

Non-compliance, even if unintentional, can have serious consequences — particularly as ASIC continues to increase its enforcement activity in this area.

In addition to this focus on preparers, ASIC has updated its guidance on matters that auditors must report. Notably, failure to lodge or late lodgement of financial statements is now classified as a significant breach of the Corporations Act and your auditor is required to report this to ASIC.

If you become aware of any past oversights or are uncertain about your obligations, then get in touch with your Accru adviser as early as possible so we can help assess the issue and support you in addressing it with ASIC, where appropriate.

Control

As mentioned above, ASIC have made various comments in relation to control and consolidation and we continue to receive a number of questions on this topic. In this section, we will consider some of the fundamental concepts around control in relation to the accounting standards and discuss some popular myths.

What is control for accounting purposes?

AASB 10 Consolidated Financial Statements is the relevant standard for determining whether an entity is a controlled entity (subsidiary) of another.

The definition of control is that an entity controls another if ‘it is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee.’

There are three elements to the definition:

- Exposure or rights to variable returns – this would include dividends, variable management fees or potential capital gains or losses.

- Power over the investee – power relates to the relevant activities of an entity and arises through voting rights, specified agreements or reliance on an entity to be able to operate.

- Ability to affect those returns – can the entity affect the variable returns to which it is entitled through the power it has over the relevant activities.

Whenever an entity assesses its control over another entity, this definition should be considered as well as the purpose and design of the investee, i.e. who established it and why.

We wanted to bust some common myths that we hear in relation to control and consolidation:

- Myth 1: You have to own more than 50% to consolidate – the definition of control does not contain a minimum voting holding to control and in assessing whether power exists, an entity should consider the spread of shareholders rather than one investor’s absolute voting rights only.

- Myth 2: Control and consolidation in the accounting standards apply only to companies – the definition of control does not specify an entity type, and the same definition is applied regardless of the type of entity. For example, Trustee companies should consider whether they control a Trust for accounting purposes.

- Myth 3: Not for profit entities do not need to consolidate – NFP entities apply the same control definition as any other entity, although there is an appendix to AASB 10 to assist NFP in assessing some of the elements.

- Myth 4: the entity is dormant, so we don’t need to consolidate – again the definition of control is universal regardless of the status of the entity. Dormant entities may have contingencies that need to be disclosed in the consolidated financial statements.

- Myth 5: the entity isn’t included in the tax consolidation so we can ignore it for the consolidated financial statements – tax consolidation and accounting consolidation are different concepts under different legislation and therefore do not form part of the same assessment.

Position papers and AI

Many of our clients undertake transactions which may be complex from an accounting perspective, it is important to document these as well as the associated accounting considerations.

We have previously discussed the preparation of position papers to support the appropriate accounting treatment and to clearly document the rationale.

These papers provide a trail for an entity to justify and support the accounting position as well as summarising the background, detailed analysis and conclusion for Boards, audit committees, external auditors and incoming finance staff.

We have noted an increase in the use of AI tools to prepare accounting position papers and make the following comments for users to note.

AI tools can be really useful to help structure position papers, summarise relevant accounting standards, and identify key disclosure requirements. However, when they are used to make technical conclusions, we often see that there is a failure to apply requirements in the standards, misunderstanding of the relevance of specific facts and circumstances or confusion where the transaction is not explicitly addressed in AASBs.

We recommend that any AI-generated content should be reviewed, challenged and cross-referenced to the AASB’s to ensure the analysis is technically sound, tailored to the specific transaction, and appropriately referenced. This quality checking will ensure that the paper you present will be of the highest quality and supportable by source documents.

Contacts

If you want any more information on any of the topics discussed in this newsletter or to discuss the application to your specific circumstances, please get in touch with your local Accru representative.