We are pleased to present the June 2026 edition of Financial Reporting Update, in this edition we will look at:

- New requirements for 30 June 2026 reporting entities

- An update on the Tier 3 NFP accounting standards

- Scope and timing of AASB 18 Presentation and Disclosure of Financial Statements

- ASIC regulatory update

- NSW Portable Long Service Leave

- Common errors – revenue

New requirements for 30 June 2026

As mentioned in the previous newsletter, there are no major changes in accounting standards for the next few reporting periods.

There are two standards for consideration at 30 June 2026, however they are likely to have little impact for most entities.

- AASB 2023-5 Amendments to Australian Accounting Standards – Lack of Exchangeability provides clarity and additional guidance for entities who transact in hyperinflationary or other currencies which might not be exchangeable, for example currencies which are not able to be taken out of their host country.

- AASB 2026-1 Amendments to Australian Accounting Standards – Disclosures about Uncertainties in the Financial Statements– additional illustrative examples added to the impairment and provisions standards to provide more guidance regarding the nature and extent of specific entity disclosures where significant uncertainties exist around inputs, estimates, assumptions and judgements.

An update on the Tier 3 NFP accounting standards

The long-awaited new standards for not-for-profit entities are getting closer, in fact the AASB Board have approved the issue of the standards, however at the time of writing they have not been issued. We are expecting an end of June release, the delay we understand is due to some administrative matters.

The two standards are:

| AASB 1061 General Purpose Financial Statements – Not for Profit Private Sector Tier 3 Entities | This standard introduces a third tier of financial reporting for certain NFP entities which includes a number of choices and simpler measurement requirements. |

| AASB 2026-2 Amendments to Australian Accounting Standards – Extending the Application of the Conceptual Framework and Limiting the Ability of Not-for-Profit Entities to Prepare Special Purpose Financial Statements | This standard will restrict the ability of NFP to prepare and lodge special purpose financial statements if the entity has: – There is a legislative requirement to prepare financial statements in accordance with accounting standards or Australian Accounting Standards OR – There is a constituting or other document that requires preparation of financial statements in accordance with Australian Accounting Standards. |

We will focus on the content of these standards in the next issue of this newsletter, however it is important to note that we will not know who needs to comply with these standards until a decision is made by the appropriate regulator as the AASB have not included any thresholds within the standards.

Scope and timing of AASB 18 Presentation and Disclosure of Financial Statements

For many of our clients, AASB 18, is a standard that is not available for adoption, however it is receiving some attention because it will shortly be applicable for Tier 1 for-profit entities, for example listed companies.

AASB 18 will replace AASB 101 Presentation of Financial Statements and will cause significant changes to the presentation of the income statement, additional disclosures around management-defined performance measures and clarification around aggregation and disaggregation and the purpose of the primary statements v the notes to the financial statements.

In Australia the release of the requirements has been staggered as follows:

| Entity type | Standard available for adoption | Effective date |

| Tier 1 for-profit entities | Yes – available on the AASB standards portal. | Mandatory for reporting periods beginning on 1 January 2027. |

| Tier 1 not-for-profit private and public sector entities | No – Although a standard is currently shown on the AASB portal, it remains subject to change following AASB deliberations and the proposals in ED 338. Accordingly, the version currently shown on the AASB portal should not be relied on. | The version on the AASB portal shows a mandatory effective date of reporting periods beginning on or after 1 January 2028, however this may be subject to change when the final standard is issued. |

| Tier 2 entities | No – AASB 1060 General Purpose Financial Statements – Simplified Disclosures for For-Profit and Not-for-Profit Tier 2 Entities is applied by Tier 2 entities, rather than AASB 101. Accordingly, until the AASB issues amendments to AASB 1060, there is no Tier 2 equivalent of AASB 18 available for adoption. | Not known at this stage. |

It is important that you understand whether there is a version of AASB 18 available for you prior to commencing any work on this new standard. In future newsletters we will provide more guidance and tips and traps to assist you in the implementation process.

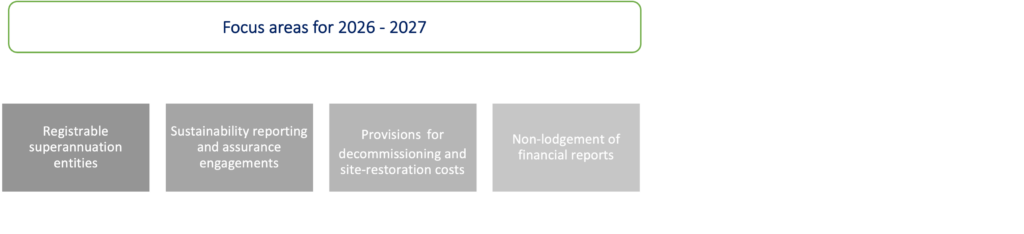

ASIC regulatory update

ASIC focus areas

ASIC have released their focus areas for reporting periods ending 30 June 2026 and 31 December 2026, they continue to retain their enduring focus areas, which are those areas requiring significant judgement and estimates:

Their specific focus areas for the current reporting period are:

Those of particular relevance to our clients are non-lodgement of financial reports (refer section below) and provisions.

The decommissioning and site-restoration focus relates to AASB 2026-1 discussed above illustrates that disclosure of provisions should cover specific judgements and estimates made in recognising and measuring provisions and not just boiler-plate statements. We encourage our readers to review disclosures throughout the financial statements to ensure they are relevant to the reported numbers and not just copied from model financial statements or accounting standards.

Non-lodgement of financial statements

ASIC has reinforced that one of their focus areas and enforcement priorities is financial reporting misconduct, including non-lodgement (on time) of financial statements.

In 2026, there has been several media releases, infringement notices and court cases relating to non-lodgement which illustrates the changes in the regulatory environment in which we are operating:

- 26-057MR Mecca companies pay $594,000 in infringement notices for failing to lodge financial reports on time (31 March 2026)

- 26-090MR Canva Group pays $792,000 in infringement notices for failing to lodge financial reports on time (6 May 2026)

- 26-111MR Fashion and beauty retailers trading under the Zara, H&M and Sephora brands pay $596,000 in infringement notices for failing to lodge financial reports on time (4 June 2026)

- 26-058MR Three public companies fined more than a million dollars for breaching financial reporting and company officer obligations (1 April 2026).

If you become aware of any breaches of lodgement requirements or are uncertain about your obligations, then get in touch with your Accru adviser as early as possible so we can help assess the issue and support you in addressing it with ASIC, where appropriate.

NSW Community Services Industry Portable Long Service Leave

This scheme commenced on 1 July 2025, making 30 June 2026 the first reporting period for which affected employers will need to consider the accounting implications of the scheme.

Under the scheme, employers are required to register community service workers, lodge service returns and pay a levy based on workers’ gross ordinary wages.

The levy rate for the 2025-26 financial year is 1.3% of gross ordinary wages, increasing to 1.7% from 1 July 2026.

For accounting purposes, employers should note that the scheme operates alongside the existing legislation and does not remove existing long service leave entitlements accrued before 1 July 2025.

There are several examples of scenarios on the long service leave website (www.longservice.nsw.gov.au) which illustrate the liabilities for different types of employees.

Common errors – Revenue

Revenue continues to be the area where we receive the most technical queries from our clients both in the for-profit and not-for-profit sectors, in this section we have discussed some common myths that still exist as well as providing some tips and traps.

Myth 1: If the contract says there are three milestones, there must be three performance obligations.

Not necessarily. Payment milestones and performance obligations are different concepts. A milestone is likely to be purely a payment mechanism rather than a transfer of a distinct good or service to the customer and therefore performance obligations need to be identified outside of the payment process.

Myth 2: If cash has been received, revenue must be recognised.

Revenue recognition is based on satisfaction of performance obligations (AASB 15) regardless of whether cash has been transferred.

If an NFP contract is within the scope of AASB 1058 then the receipt of cash (and therefore obtaining control of an asset) is likely to result in the recognition of revenue.

Myth 4: An acquittal report is a performance obligation.

Generally, acquittal reports, progress reports and administrative reporting requirements are evidence of compliance with a funding agreement rather than a promised good or service transferred to the funder. This means that they will not normally meet the definition of a performance obligation under AASB 15.

Myth 5: A grant is sufficiently specific because the purpose is clearly stated.

A broad objective such as “improve community wellbeing” or “support disadvantaged youth” on its own is not sufficiently specific. The agreement (or related document) needs to specify the promised goods or services in enough detail that it can be determined when they have been transferred.

We find that clients also fall into the following traps:

- Ignoring promises that are implied rather than written.

Performance obligations can arise from customary business practices, published policies or specific representations made to customers, not just from the written contract.

- Focusing only on legal form / terminology.

A key accounting concept is substance over legal form. A legal agreement calling something a “grant”, “donation”, “membership fee” or “service agreement” does not determine the accounting treatment.

- Assuming revenue is recognised evenly because funding is received evenly.

Revenue is recognised based on the transfer of promised goods or services, which may be over time, at a point in time, or in a pattern that differs from the funding receipts. Remember that criteria must be met to be able to recognise revenue over time – it is not automatic under AASB 15.

Contacts

If you want any more information on any of the topics discussed in this newsletter or to discuss the application to your specific circumstances, please get in touch with your local Accru representative.