BUSINESS TAXATION

Although the Australian economy has made a remarkable recovery to date, the Government is still committed to incentivising businesses to spend and innovate, offering tax cuts which they expect to lead to jobs growth. Some of the announcements are extensions of last year’s Budget measures and other are new initiatives.

Instant asset write-off / Temporary full expensing of assets extended

Last year’s announcement of full expensing of depreciable assets for businesses with turnover under $5 billion was one of the biggest Budget outlays ever made. It has now been extended for a further 12 months.

Full expensing in the year of first use applies to new depreciable assets and the cost of improvements to existing eligible assets. For small and medium sized businesses (with aggregated annual turnover of less than $50 million), full expensing also applies to second-hand assets.

Temporary full expensing will be extended to allow eligible businesses with aggregated annual turnover or total income of less than $5 billion to deduct the full cost of eligible depreciable assets of any value, acquired from 7:30pm AEDT on 6 October 2020 and first used or installed ready for use by 30 June 2023.

This measure doubles as an incentive for businesses to purchase new equipment, whilst also presenting a marketing opportunity for businesses of all sizes which supply depreciable assets.

Carry back tax losses

Another initiative announced last year that has been extended for another year. The Government will allow eligible companies to carry back tax losses from the 2022-23 income years to offset previously taxed profits in 2018-19 or later income years when they lodge their 2022-23 tax return.

Corporate tax entities with an aggregated turnover of less than $5 billion can apply tax losses against taxed profits in a previous year, generating a refundable tax offset in the year in which the loss is made. The tax refund would be limited by requiring that the amount carried back is not more than the earlier taxed profits and that the carry back does not generate a franking account deficit. The tax refund will be available on election by eligible businesses when they lodge their 2020-21, 2021-22 and now 2022-23 tax returns.

‘Patent box’ tax concession for Australian medical and biotech innovations

The Government will introduce a patent box tax regime to further encourage innovation in Australia by taxing corporate income derived from patents at a concessional effective corporate tax rate of 17 per cent, with the concession applying from income years starting on or after 1 July 2022.

The patent box will apply to income derived from Australian medical and biotechnology patents. The Government will also consult on whether a patent box would be an effective way of supporting the clean energy sector.

The requirement for domestic development will encourage additional investment and hiring in research and development activity and encourage companies to develop and apply their innovations in Australia. The Government will consult with industry before settling the detailed design of the patent box.

Employee Share Scheme (ESS) changes

The Government will remove the cessation of employment taxing point for the tax- deferred Employee Share Schemes (ESS) that are available for all companies. This change will apply to ESS interests issued from the first income year after the date of Royal Assent of the enabling legislation.

Currently, under a tax-deferred ESS, where certain criteria are met employees may defer tax until a later tax year (the deferred taxing point). The deferred taxing point is the earliest of:

- cessation of employment

- in the case of shares, when there is no risk of forfeiture and no restrictions on disposal

- in the case of options, when the employee exercises the option and there is no risk of forfeiting the resulting share and no restriction on disposal

- the maximum period of deferral of 15 years.

This change will result in tax being deferred until the earliest of the remaining taxing points. The Government will also reduce red tape for ESS by:

- removing regulatory requirements for ESS, where employers do not charge or lend to the employees to whom they offer ESS

- where employers do charge or lend, streamlining requirements for unlisted companies making ESS offers that are valued at up to $30,000 per employee per year.

This measure will help Australian companies to engage and retain the talent they need to compete on a global stage, consistent with recommendations from the Global Business and Talent Attraction Taskforce.

Self-assessing effective life of intangible depreciating assets

The Government will allow taxpayers to self-assess the tax effective lives of eligible intangible depreciating assets, such as patents, registered designs, copyrights and in- house software. This measure will apply to assets acquired from 1 July 2023, after the temporary full expensing regime has concluded.

Division 7A (non)update

Changes to Division 7A have been announced dating back to the 2016-17 Budget and no doubt further consultation is needed before the final changes can be introduced as law. The start date for these changes has now been changed from 1 July 2020 to be the income year commencing on or after the date of Royal Assent of the enabling legislation.

Digital Economy Strategy

The Government announced $1.2 billion funding over 6 years from 2021-22 for a Digital Economy Strategy to support Australia to be a leading digital economy and society by 2030. In summary, it includes support for the following priorities:

- Enhancing Artificial Intelligence capability

- Investing in emerging aviation technologies

- Investment incentives, including a 30% refundable Digital Games Tax Offset for qualifying expenditure after 1 July 2022

- Unlocking the value of data

- Digital infrastructure and skills

- Enhancing Government Services delivery

- Small and Medium Enterprise digitalisation

- Improving safety security and trust

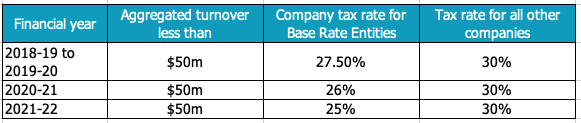

Corporate Tax Rate – reminder

The Government remains committed to the 10 year enterprise tax plan announced five years ago. Attempts to extend the corporate tax cuts to companies over $50 million have failed thus far, but presumably the Government will continue to make efforts to pass them.

They have succeeded in bringing forward the tax cut for “Base Rate Entities”. A Base Rate Entity for 1 July 2018 onwards has aggregated turnover below $50 million and that has 80% or less of their assessable income as ‘base rate entity passive income’

Therefore, the current corporate tax rates are as follows:

The company tax rate for Base Rate Entities is also the applicable rate for franking credits attached to franked dividends.

EMPLOYMENT INCENTIVES

JobTrainer Fund extension

The Government has pledged to deliver around 163,000 additional low fee and free training places in areas of skills needs, including 33,800 training places to support aged care skills needs and 10,000 places for digital skills courses. The additional funding of $500 million is essentially dependent on the States and Territories matching the $500 million contribution.

Boosting apprenticeships wage subsidies

The Government is building on and expanding the apprenticeship wage subsidies announced in last year’s Budget. The additional funding is in place over 4 years and in place to support businesses and Group Training Organisations to take on new apprentices and trainees. This measure will uncap the number of eligible places and increase the duration of the 50 per cent wage subsidy to 12 months from the date an apprentice or trainee commences with their employer.

From 5 October 2020 to 31 March 2022, businesses of any size can claim the Boosting Apprenticeship Commencements wage subsidy for new apprentices or trainees who commence during this period. Eligible businesses will be reimbursed up to 50 per cent of an apprentice or trainee’s wages of up to $7,000 per quarter for 12 months.

Changes to temporary visas to support workforce participation

The Government is temporarily allowing workers on student visas to work more than 40 hours per fortnight, provided they are employed in tourism, hospitality or agricultural sectors.

The Government has removed the requirement for applicants for the Temporary Activity visa (subclass 408) to demonstrate their attempts to depart Australia if they intend to undertake agricultural work. The period in which a temporary visa holder can apply for the Temporary Activity visa has also been extended from 28 days prior to visa expiry to 90 days prior to visa expiry.

See our separate coverage on Federal Budget changes announced affecting individuals and superannuation, If you would like to know more about how the Federal Budget announcements affect your business, please get in touch with your local Accru advisor.