INDIVIDUALS

Low and Middle Income Tax Offset

The only change to individual tax rates for many taxpayers was the extension for another year of the Low and Middle Income Tax Offset of $1,080, along with the enhanced Low Income Tax Offset (now $700 rather than previous $445). This was due to expire 30 June 2021.

The offset applies as follows to the following income levels:

Personal tax rates

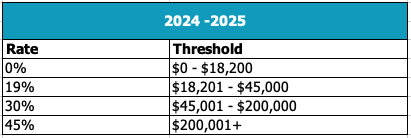

Rumours of bringing forward the next stage of personal tax cuts proved to be unfounded. The third and final stage of changes to personal tax rates announced is still intended to occur from 1 July 2024 and will result in reducing the 32.5% tax rate down to 30% and applying this to taxable incomes ranging from $45,000 – $200,000, meaning 94% of taxpayers will not pay more than 30%.

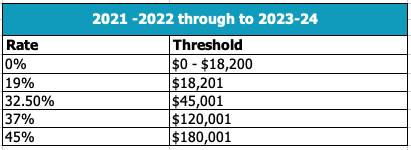

Resident tax rates for financial years commencing 1 July 2020, 2021, 2022 and 2023 remain:

Medicare is an additional 2% where applicable, so the top marginal rate is effectively 47%

Based on Budget announcements resident tax rates from 2024-25 will become:

Modernising individual tax residency rules

In a welcome move, the Government announced they will replace the individual tax residency rules with a new, modernised framework. The primary test will be a simple ‘bright line’ test — a person who is physically present in Australia for 183 days or more in any income year will be an Australian tax resident. Individuals who do not meet the primary test will be subject to secondary tests that depend on a combination of physical presence and measurable, objective criteria.

The measure will have effect from the first income year after the date of Royal Assent of the enabling legislation. The new framework, based on recommendations made by the Board of Taxation in its — a model for modernisation, will be easier to understand and apply in practice, deliver greater certainty, and lower compliance costs for globally mobile individuals and their employers.

First home buyers and builders

In support of the Australian dream of home ownership in a housing market that continues to challenge that dream, the Government has announced a Housing Package with the following key features:

- The HomeBuilder program extends the construction requirement from six months to 18 months for all existing applicants, to smooth out the work across 2021 and 2022

- Establishing a Family Home Guarantee with 10,000 places to support single parents with dependents to enter or re-enter the housing market with a deposit of as little as 2%

- Extending the First Home Loan Deposit Scheme to provide an additional 10,000 New Home Guarantees in 2021-22 to allow eligible first home buyers to build a new home or purchase a newly constructed home sooner with a deposit of as little as 5%.

- The Government will increase the maximum releasable amount of voluntary contributions under the First Home Super Saver Scheme (FHSSS) from $30,000 to $50,000. Voluntary contributions made from 1 July 2017 up to the existing limit of $15,000 per year will count towards the total amount able to be released. The increase will apply from the start of the first financial year after Royal Assent of the enabling legislation, expected to have occurred by 1 July 2022.

Women’s Economic Security Package

The Government is building on prior women’s security initiatives by providing $3.4 billion over five years to improve women’s workforce participation and economic security. Funding includes:

- $1.7 billion over five years from 2020-21 (and $671.2 million per year ongoing) to assist families by reducing out of pocket costs and supporting parental choice through increasing the Child Care Subsidy (CCS) rate by 30 percentage points for the second child and subsequent children aged five years and under in care, up to a maximum CCS rate of 95 per cent for these children, commencing on 11 July 2022; and removing the CCS annual cap of $10,560 per child per year commencing on 1 July 2022

- $42.4 million over seven years from 2021-22 to establish the Boosting the Next Generation of Women in Science, Technology, Engineering and Mathematics (STEM) Program by co-funding scholarships for women in STEM in partnership with industry

- $38.3 million over five years from 2021-22 to increase grant funding available through the Women’s Leadership and Development Program

- $13.9 million over four years from 2021-22 to establish an Early Stage Social Enterprise Foundation focused on providing capacity building and financial support for early stage social enterprises that improve the safety and economic security of Indigenous women

- $12.2 million over two years from 2021-22 to fund an additional round of the National Careers Institute Partnership Grants program to support projects that facilitate career opportunities and career pathways for women

- $10.7 million over two years from 2021-22 to extend the family law small claims property pilot and Legal Aid Commission family law property mediation trial for settlement of property of less than $500,000 following a relationship breakdown

- $2.6 million over three years from 2021-22 to expand the Career Revive program to support more medium to large regional businesses attract and retain women returning to work after a career break

- $0.6 million over three years from 2021-22 for the Women in STEM Ambassador to develop an evaluation toolkit to support standardised evaluation planning and reporting tools for the STEM sector in the evaluation of STEM gender equity initiatives. Funding for this will be met from within the existing resources of the Department of Industry, Science, Energy and Resources

- expanding the Mid-Career Checkpoint Program to Victoria, beyond existing pilots in Queensland and New South Wales, and expanding eligibility to include people who have been absent from work due to caring responsibilities for six months or more and existing workers at risk of unemployment, primarily targeting female dominated, COVID-19 affected industries. Training grants of up to $3,000 will also be available to support skills and training needs to increase employability and support career advancement. Funding for this will be met from within the existing resources of the Department of Education, Skills, and Employment.

SUPERANNUATION

A number of changes announced to superannuation this year are intended to remove restrictions on people making contributions into superannuation, without actually increasing the amounts that people can hold in super. There is no increase in the caps on Total Super Balance, with existing limits remaining as they are, including the indexation to the Transfer Balance Cap and contribution limits.

No threshold for superannuation guarantee

Currently, a worker who earns less than $450 per month is not eligible for superannuation guarantee. This monthly threshold of $450 for eligibility for superannuation guarantee will be abolished from the start of the first financial year after Royal Assent of the enabling legislation, expected to occur prior to 1 July 2022.

Reducing eligibility for Downsizer Contributions from age 65 to age 60

Downsizer contributions have been in place for several years and are designed to encourage older Australians to consider downsizing their house, freeing up the stock of larger homes for younger families.

Provided the house is at least partially covered by the main residence exemption and has been owned for over 10 years, the downsizer contribution allows people to make a one-off, post-tax contribution to their superannuation of up to $300,000 per person from the proceeds of selling their home. Both members of a couple can contribute in respect of the same home, and contributions do not count towards non-concessional contribution caps.

The Government will reduce the eligibility age to make downsizer contributions into superannuation from 65 to 60 years of age. This will have effect from the start of the first financial year after Royal Assent of the enabling legislation, expected to have occurred prior to 1 July 2022.

Removing the work test for voluntary superannuation contributions

The Government will allow individuals aged 67 to 74 years (inclusive) to make or receive non-concessional (including under the bring-forward rule) or salary sacrifice superannuation contributions without meeting the work test, subject to existing contribution caps. Individuals aged 67 to 74 years will still have to meet the work test to make personal deductible contributions.

The measure will have effect from the start of the first financial year after Royal Assent of the enabling legislation, expected to have occurred prior to 1 July 2022. Currently, individuals aged 67 to 74 years can only make voluntary contributions (both concessional and non-concessional) to their superannuation, or receive contributions from their spouse, if they are working at least 40 hours over a 30 day period in the relevant financial year.

Self-managed Super Funds legacy retirement product conversions

The Government will allow individuals to exit a specified range of legacy retirement products, together with any associated reserves, for a two-year period. The measure will have effect from the first financial year after the date of Royal Assent of the enabling legislation. The measure will include market-linked, life-expectancy and lifetime products, but not flexi-pension products or a lifetime product in a large APRA-regulated or public sector defined benefit scheme.

Currently, these products can only be converted into another like product and limits apply to the allocation of any associated reserves without counting towards an individual’s contribution caps. This measure will permit full access to all of the product’s underlying capital, including any reserves, and allow individuals to potentially shift to more contemporary retirement products.

Increased flexibility for Self-managed Super Fund and Small APRA Fund residency

The Government has announced that it will extend the safe harbour test for central management and control from two years to five years and also remove the active member test. This allows members who are temporarily overseas to keep and continue their contributions to their preferred fund.

Changes in superannuation caps and thresholds

Although not part of the Federal Budget announcements, it is worth a reminder that on 1 July 2021 indexation will occur for the following superannuation caps:

- Concessional contribution cap goes from $25,000 to $27,500

- Non-concessional contribution cap goes from $100,000 to $110,000

- Bring forward concessional contribution cap goes from $300,000 to $330,000. However any bring forward caps triggered before 1 July 2021 are still limited to $300,000 and cannot access any of the increase

Furthermore, the Transfer Balance Cap increases from $1,600,000 to $1,700,000. It is important to note that this is not a uniform increase and that people that have commenced account-based pension prior to 1 July 2021 can only access the proportion of the increase that was unused at pension commencement. As an example, if the original account-based pension commenced at $800,000, then the increase in the indexed cap available is: $800,000 / $1,600,000 x $100,000 = $50,000. The Transfer Balance Cap in this example would be increased to $1,650,000.

See our separate coverage on Federal Budget 2021 announcements affecting businesses. If you would like to know more about how the Federal Budget announcements could you and your superannuation, please get in touch with your local Accru advisor.